SVB Failure: The Impact on Private Credit

Share

We believe this event will tighten the availability of credit as small and mid-sized banks similar to SVB shore up their balance sheets to encourage shareholder confidence. We also believe the event will have significant consequences for credit market structure. Specifically, we anticipate regulators will tighten oversight of medium-sized banks, leading to reduced credit availability for higher-yield borrowers. Finally, we expect depositors to move more of their balances from smaller to larger banks. Since large banks tend to make larger loans, we believe smaller businesses will find it disproportionately harder to access bank credit.

The upshot is that the SVB collapse is a trigger we believe will further accelerate the transition of credit away from banks and into the private markets, especially for smaller businesses.

Bank Credit Availability Will Tighten

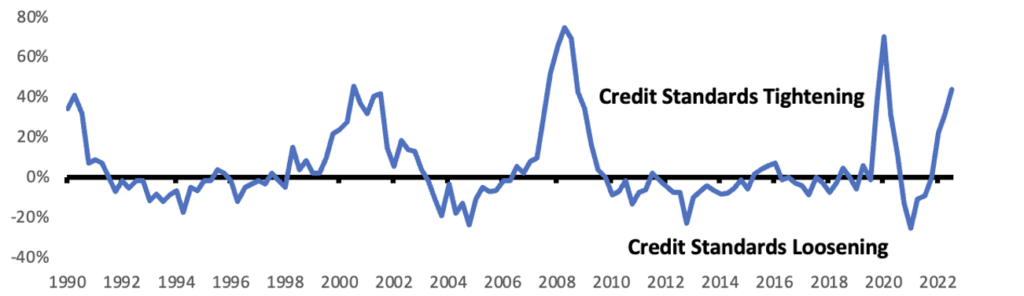

Coming into the events of March 2023, banks were already tightening credit standards for clients because of recession risk and persistent inflation. Each quarter, the Federal Reserve surveys bank loan officers to understand changes to their credit standards over the prior quarter. For the fourth quarter of 2022, the net tightening of credit standards represented the worst reading—absent the Covid blip in 2020—since the Great Financial Crisis.

Net % of Loan Officers Tightening Credit Standards for Small and Medium-Sized Businesses

Source: Board of Governors of the Federal Reserve System, Senior Loan Officer Opinion Survey and FRED Economic Data (fred.stlouisfed.org/series/DRTSCIS)

With the collapse of SVB, we believe banks will further tighten lending standards to ensure they are not the next target for a bank run. Though SVB’s failure was primarily due to poor asset liability matching, no bank will want to show vulnerability and provoke their own bank run. While it’s nearly impossible for banks to immediately change the risk characteristics of a loan portfolio, we expect newly issued loans to undergo intense scrutiny and many current borrowers to struggle to extend existing lines of credit.

Bank Regulation Will Tighten

In 2018 Congress passed the Economic Growth, Regulatory Relief and Consumer Protection Act. This loosened the Dodd-Frank requirements for mid-sized banks between $50bn and $250bn in assets. While Congress will likely not reverse course, the bill did provide the Fed flexibility in how they regulate these mid-sized banks. We expect the Fed will significantly tighten their regulatory approach towards mid-sized banks, which will likely rein in their riskier loan portfolios.

Depositor Flight to Large Banks Will Make It Harder for Smaller Businesses to Obtain Loans

On March 9 alone, SVB experienced $42bn in withdrawals,[1] or about 24% of their $175bn in total deposits as of Q4 2022.[2] Three days later, the Federal Deposit Insurance Corporation (FDIC) put Signature Bank, with $89bn in deposits,[3] into receivership. The affected depositors, along with many other skittish depositors at small and medium-sized banks, are moving their deposits to other banks. Anecdotal evidence suggests that large banks were flooded with new account applications the Monday following the SVB collapse.

We expect that many of these deposits will find their way to large, stable, highly regulated banks. These banks, many of which are designated Global Systematically Important Banks (GSIB), are significantly entwined in the global economy, causing many to believe they have an implicit regulatory backstop should they show signs of weakness. Depositors will put a premium on this stability.

What will these large banks do with the deposit inflows? Historically, large banks make larger loans, and we don’t see any reasons for that trend to reverse course. As a result, large borrowers stand to benefit while smaller borrowers will likely struggle to find credit from their bank partners.

Average Loan Size - Small Banks vs. All Banks

Source: Board of Governors of the Federal Reserve System (US) and FRED Economic Data (fred.stlouisfed.org/series/EAANQ, fred.stlouisfed.org/series/EAAXSSNQ)

Closing Thoughts: Private Credit Will Fill the Void

In summary, we expect tighter bank lending standards, restrictive regulation on medium-sized banks, and a flow of deposits from small and mid-sized banks into large megabanks. The result could potentially be a significant reduction in the availability of bank credit to small borrowers.

We believe the main beneficiary of this dynamic will be private lenders, unconstrained by shifts in bank regulatory regimes and flighty depositors. Private credit managers will have greater access to borrowers and more negotiating power when structuring loans. The trend from banks to private markets, already in progress over the last decade, is likely to quicken its pace in the years ahead.

Sources

[1] dfpi.ca.gov/wp-content/uploads/sites/337/2023/03/DFPI-Orders-Silicon-Valley-Bank-03102023.pdf?emrc=bedc09

[2] fdic.gov/news/press-releases/2023/pr23016.html

[3] fdic.gov/news/press-releases/2023/pr23018.html

Disclosures

This market commentary was prepared by Alternative Fund Advisors, LLC (“AFA”). The information set forth herein has been obtained or derived from sources believed by AFA to be reliable. However, AFA does not make any representation or warranty, express or implied, as to the information’s accuracy or completeness, nor does AFA recommend that the attached information serve as the basis of any investment decision. The views expressed reflect the current views as of the date hereof. This document has been provided to you solely for information purposes and does not constitute an offer or solicitation of an offer, or any advice or recommendation, to purchase any securities or other financial instruments, and may not be construed as such.

AMCLX is a closed end interval fund. An investment in the Fund involves risk. The Fund’s investment in private credit companies is speculative and involves a high degree of risk, including the risk associated with leverage.

Past performance does not guarantee future results.

Current and future holdings are subject to risk.

Distributed by Foreside Services, LLC